Imagine, for a moment, that you are standing at your warehouse loading dock on a Tuesday morning. A flatbed truck is pulling away, carrying $250,000 worth of your high-grade raw materials specialized electronic components, custom-molded plastics, and precision-engineered steel. That truck isn’t heading to a customer; it’s heading to a partner vendor 100 miles away.

As the taillights fade into the distance, a familiar knot forms in your stomach. For the next three weeks, those materials your company’s hard-earned assets essentially vanish from your sight. In many systems, they might show as shipped, but can you say with 100% certainty what they are worth right now? If your bank called today to audit your assets, could you prove that those materials are still yours, or have they already been “consumed” in a ledger somewhere, months before the finished goods return?

This is the Black Box of Subcontracting. For many growing businesses, subcontracting is a vital tool for scaling production without the massive overhead of new machinery. However, without mastering the underlying logic of how these goods move and are valued, that growth comes at a steep price: the loss of financial control.

The Annex Strategy: Redefining Ownership in Transit

To solve the subcontracting puzzle, we have to start with a shift in perspective. Most businesses treat a subcontractor as a supplier someone you send a Purchase Order to and receive an invoice from. But from an inventory and accounting standpoint, that mindset is a trap. When you ship raw materials to a vendor for processing, you haven’t “sold” them anything. You are simply moving your property to a different room.

Think of your subcontractor’s facility not as an outside company, but as a Virtual Annex of your own warehouse. This distinction is vital for your business value. It ensures your company’s total asset value is always accurate a detail your bank, your tax accountant, and your investors care about deeply.

In a high-functioning business logic, those materials stay on your balance sheet as Inventory even while they are being welded, painted, or assembled 100 miles away. This isn’t just a technicality; it’s a matter of Asset Integrity. If your records treat that shipment as a sale or a loss, your balance sheet is lying to you. By maintaining a digital mirror of the subcontractor’s floor, you ensure that every dollar of raw material remains accounted for until the very second it is transformed into a finished product.

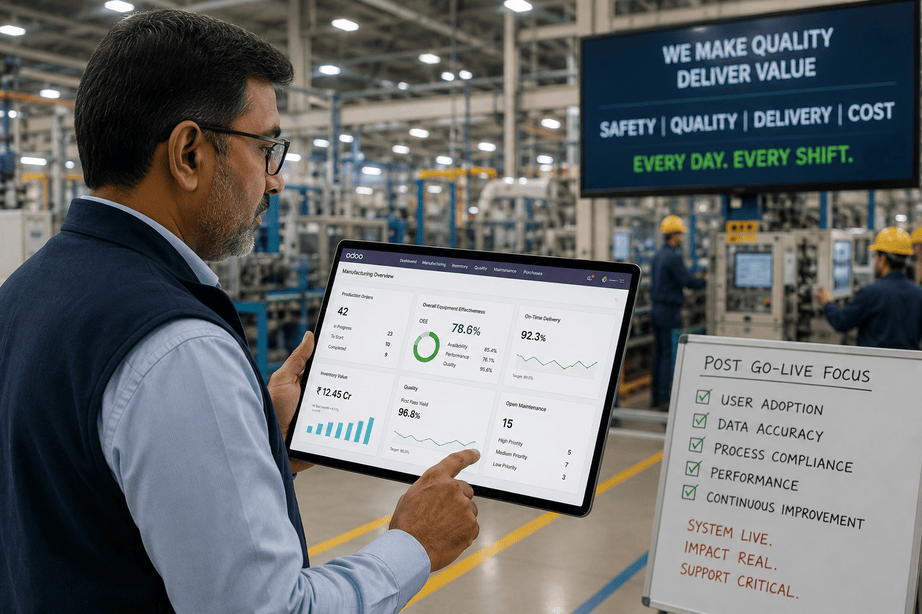

The Financial Rollercoaster: Why Balance Sheets Dip

When we look at the financial health of a manufacturing firm, the Chief Financial Officer (CFO) is often the first to notice when subcontracting logic fails. A common frustration in the executive suite is the “valuation dip.” This occurs when large batches of inventory are sent out, and the system immediately expenses them or removes them from the asset list. On paper, it looks like the company has suddenly lost thousands of dollars in assets, only for that value to miraculously reappear weeks later when the finished goods arrive.

This rollercoaster makes monthly reporting a nightmare and can lead to serious miscommunications with stakeholders. The solution lies in understanding that the value of the components must be accrued into the finished good. The valuation of the incoming product must follow a strict mathematical logic: Total Value = Cost of Materials + Service Fee + Landed Costs.

By automating this transition, the “dip” vanishes. The value simply transforms from “Raw Materials” to “Work-in-Progress” and finally to “Finished Goods,” keeping the balance sheet flat and accurate throughout the cycle. This ensures that the $100 of material “disappears” from your raw stock and “reappears” inside the value of the finished product. Your part is now worth $150 on your shelf, and your financial reports stay 100% accurate in real-time.

The Scrap Trap: Navigating the Nightmare of Phantom Inventory

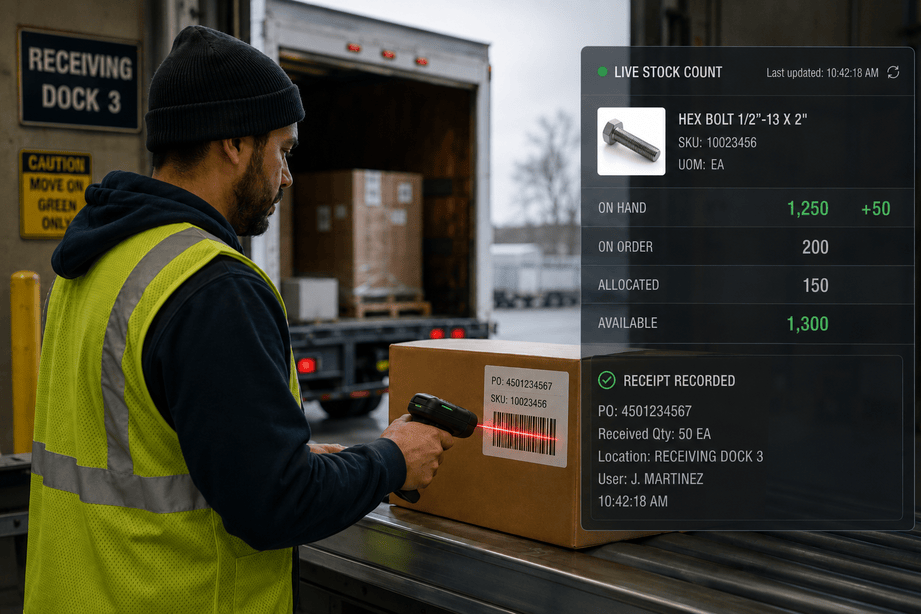

While the finance team worries about the balance sheet, the Director of Operations is often dealing with a more physical headache: Phantom Inventory. This is the dangerous scenario where your computer thinks you have stock that was actually thrown in a scrap bin weeks ago at a vendor’s facility.

Standard manufacturing planning assumes a perfect world where one unit of raw material equals one unit of finished product. But in reality, waste happens. A vendor might have a machine error and use 110 pieces of a component to make 100 finished units. If your system is set to a static logic meaning it only records exactly what the recipe calls for you are left with 10 units of “phantom” stock in your records.

Mastering this requires a shift toward Flexible Consumption. When the finished goods are received, the system must allow the person on the loading dock to record exactly what was used, not just what was planned. By matching the consumption of raw materials directly to the receipt of finished goods, you keep your stock levels honest. This ensures your reordering triggers are reliable and you aren’t accidentally running out of materials you thought you still had sitting at a vendor’s shop.

Proactive Planning: Ending the Stock-Out Phone Call

Production planners live in a world of constant coordination. One of their greatest struggles is the “blind spot” created by off-site inventory. David, a lead planner I recently spoke with, described the frustration of waiting for a subcontractor to call saying they are out of bolts, only to realize the bolts have a two-week lead time.

The “Annex” mindset solves this by providing true Supply Chain Visibility. When the subcontractor’s site is treated as a tracked location within your own ecosystem, you can set “Reordering Rules” specifically for that site. When the stock levels at the vendor’s shop drop below a certain threshold, the system triggers a resupply movement or a purchase order automatically. You are no longer managing by phone call; you are managing by data. This proactive stance prevents production delays and ensures that your vendors are never sitting idle while waiting for materials that should have been sent days ago.

The True Cost of Production: Why Freight is an Asset

One often-overlooked area where control is lost is in the logistics. If it costs $2,000 to ship the raw materials to the vendor and another $2,000 to get the finished goods back, that $4,000 is part of the product’s value. It is not just an administrative expense to be buried in a general ledger.

If you don’t include these Landed Costs in your product valuation, you are understating the value of your inventory and overstating your expenses for the month. Mastering the logic means attaching these freight bills to the specific receipt of goods. This ensures that your Cost of Goods Sold (COGS) is accurate down to the penny when that item is finally sold to a customer.

From a leadership perspective, this is about Margins. When you have total control over your subcontracting costs including the materials, the labor, and the shipping you know exactly how much profit you make on every single unit. You can see if a specific vendor is becoming too wasteful or if your logistics costs are eating your dividends.

Traceability: The DNA of Your Product and Brand

In today’s market, control isn’t just about dollars and cents – it’s about Accountability and Risk Management. For companies in industries like aerospace, medical devices, or food and beverage, the “Black Box” isn’t just a financial risk; it’s a legal one.

If a component fails in the field, you need to know exactly which batch of raw material was used and which vendor touched it. When you send materials to a subcontractor, you must maintain the Lot or Serial Number chain. The logic here is Parent-Child tracking. Your system should be able to tell you: “This finished unit (Serial #501) was made using Steel Batch #A22, which was processed by Vendor X on Tuesday.”

Without this, you don’t have control; you have a liability. By forcing the recording of lots during the “Receive” step, you create a digital thread that protects your business from the catastrophic costs of a blind recall. This level of traceability builds immense trust with high-tier customers who demand to know every detail of their supply chain.

Data Integrity as a Competitive Advantage

In the modern manufacturing landscape, the winners aren’t just the ones who make the best products; they are the ones who have the best data. Subcontracting is a brilliant way to stay lean and agile, allowing you to scale up or down without the burden of heavy machinery. However, that agility is only an asset if it’s backed by transparency.

When you master the logic of sending raw materials and receiving finished goods, you aren’t just doing “data entry.” You are building a transparent, audited, and highly accurate financial engine. You can look at your balance sheet with confidence, knowing that every dollar is accounted for, whether it’s sitting on your shelf or on a truck 100 miles away.

Summary of Strategic Business Value

- Asset Protection: Raw materials remain on your books as current assets until the final product is received, ensuring a healthy and accurate balance sheet.

- Margin Accuracy: By combining material costs, service fees, and freight into one valuation, you get a true picture of your profitability per unit.

- Operational Reliability: Real-time visibility into vendor stock levels prevents emergency shipments and production downtime.

- Risk Mitigation: Full traceability ensures that your brand is protected in the event of a quality issue or recall.

- Clean Data: Eliminating phantom inventory ensures that your purchasing decisions are based on reality, not on system errors.

Subcontracting should be a tool for growth, not a source of confusion. By opening the Black Box and illuminating it with the light of accurate, real-time logic, you turn a logistical challenge into a competitive advantage. You can send those materials out the door with total confidence, knowing exactly what they’re worth every step of the way.

A Closing Thought for Your Next Operations Meeting:

As you look at your current external production, do you feel confident that your system captures the full cost of a product? If you had to recall a specific batch of raw materials today, could you identify which finished products at your subcontractor’s site contain those materials within the next ten minutes? If the answer is no, it might be time to rethink the logic of your Black Box.